Can You Contribute to an Ira and a 401k

401k

The 401k is a retirement savings programme that's normally sponsored by your employer. An eligible employee can make pre-tax contributions through payroll deductions. (Some plans have the option to contribute with after-taxation income.) Here are the advantages of the 401k plan.

- You lot'll pay less revenue enhancement today. Your contributions won't be taxed and it will grow tax-free. You lot will pay taxes when you withdraw it later.

- The contributions volition be taken out of your paychecks. It won't pass through your checking business relationship so you lot won't exist tempted to utilise it. This is the easiest way to invest.

- Many employers offer matching program up to a sure percent of your salary. So if your employer matches 5% of your salary, so your contributions will instantly double (upwardly to v% of your bacon.)

- The 2022 maximum contribution is $19,000.

Roth IRA

The Roth IRA is another retirement savings account. Still, you have to manage it yourself. When I first started working, I opened a Roth IRA with Firstrade considering their fees were very low. They're even better now. The online trading fee is $0 fifty-fifty for mutual funds! Here are some advantages of the Roth IRA.

- You invest with after-taxation money. The keen thing is yous volition never have to pay any tax on the gains.

- You can withdraw your contributions anytime with no revenue enhancement or penalty.

- Y'all tin invest in annihilation you like. Usually, the 401k has limited options.

- In 2019, the maximum contribution is $6,000.

Read more than – How to start contributing to a Roth IRA.

Early withdrawal

The dazzler of these two retirement accounts is that y'all can use them in tandem to avoid the 10% early withdrawal penalization. They will come in very useful if y'all plan to retire early. Y'all tin read more than almost this process – Build a Roth IRA ladder to minimize taxes in early retirement.

Should I invest in the 401k or Roth IRA?

Ideally, you should contribute the maximum to both the 401k and Roth IRA. However, most new investors don't take that much income. To max out both accounts, you lot'd need to salvage $25,000. That's a lot of money. If yous can't save that much, then do this.

First, contribute to the 401k upward to the employer matching. This is the best investment yous can make considering your investment will double correct away. If you're not contributing this much, you're giving upwardly free money. Let's calculate and see where to invest after that. I'll use an excel spreadsheet to do this.

Hither are some assumptions.

- The investor is in the 22% tax bracket. He can invest $6,000 in Roth IRA or $7,690 pretax in 401k.

- 8% almanac gain.

- The investor starts at 22, retires at 60, and lives until 86.

- The withdrawal rate is 7% at threescore. I made the money run out at 86.

- After retirement, the investor will have a lower effective tax charge per unit due to non having a chore. I assume the investor will pay 12% tax. This is a large assumption, merely information technology should be valid. Nearly retirees make less money after they retire and pay less tax.

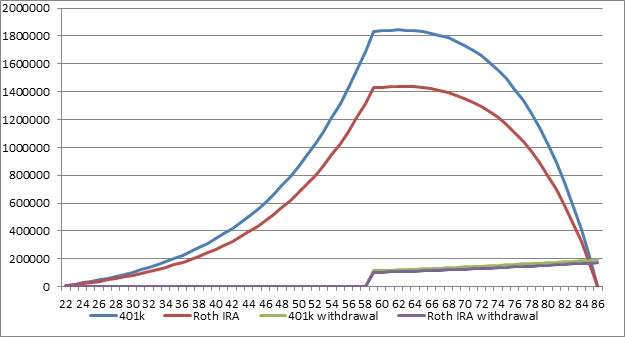

Here is the graph of the 401(thou) vs Roth IRA.

As we expected, the 401(chiliad) portfolio grows much more than than the Roth IRA. That'due south because you don't have to pay revenue enhancement initially and can invest more. The 401k grows to $ane,829,768 past the fourth dimension we're 60 years erstwhile. The Roth IRA grows to $1,427,647. That's a big divergence.

Withdrawal

We need to zoom into the withdrawal period to see the differences betwixt the ii. This graph shows the income later tax.

Nosotros tin can see the 401k comes out alee.

- 401k: full $four,214,958 before portfolio depletion (subsequently 12% tax)

- Roth IRA: total $three,737,107 earlier portfolio depletion (after 0% taxation)

That's near half a million dollars more if you invest in the 401k.

Why does the 401k come out then far ahead? The big divergence is due to the subtract in the tax bracket. The 401k has an advantage considering we assume the revenue enhancement rate will be lower later retirement. I assume if you pay tax now, you'll pay 22%. Later on retirement, yous'll pay 12%. That's the secret sauce.

Still, if your tax rate will be college after retirement, then the Roth IRA will win. Some people think the tax rate will increase in the time to come, only I disagree. Low-income workers already struggle mightily to brand ends meet. Increasing tax at the lower brackets will brand life a lot more hard for them. I think the higher tax brackets will see more change.

What if you lot're in the same tax subclass after retirement

*This section is a follow up to a comment.

The 401k is clearly improve if you're in the lower tax subclass later retirement, just what if you're in the same tax bracket? The 401k will nonetheless come out alee due to subtlety in the tax lawmaking.

Let's practice an example of a childless family making $150,000 per twelvemonth.

When they contribute to the 401k, they salve 22% in taxes right away.

Later this family retires, they still generate $150,000 from withdrawal. They will exist in the same taxation bracket every bit before retirement. However, their effective taxation rate is 13%.Their effective tax rate is lower than their marginal taxation rate. The $150,000 income is taxed at dissimilar rates as you move up the brackets.

- 10% for $0 – $19,400

- 12% for $xix,400 – $78,950

- 22% for $78,950 – $168,400

There is a spread of 9% in the tax charge per unit even if they make the aforementioned amount of money later retirement. The 401k still come out alee. That'due south the divergence between effective taxation rate and marginal tax rate. If this is confusing, you should read upward on the deviation betwixt the two.

- Effective taxation rate = full revenue enhancement / taxable income.

- Marginal tax rate = the percent taken from your next dollar of taxable income.

For us, nosotros should be in a lower revenue enhancement subclass after retirement. Our effective revenue enhancement rate will be around 7%. That's a huge spread of 15%. I seriously incertitude the tax code volition change that much, only who knows.

401k first

In conclusion, it's better to max out your 401k first and then work on the Roth IRA. Most of us volition be in the lower tax bracket afterwards retirement. Assuming your 401k programme is good, it's best to go with the 401k first. Of class, it's all-time to max out both your 401k and Roth IRA as soon as you can. That's the best of both worlds.

*The but reason to non become with the 401k get-go is this. If your 401k is really bad and the employer doesn't match. In that case, you tin can open a traditional IRA and skip the 401k.

Okay, what do you retrieve? I dearest my 401k because motorcar deduction makes investing and so piece of cake. It's the all-time way to invest, peculiarly for beginners. The Roth IRA is really expert too. That's why I invest in both of them.

*Sign up for a free account at Personal Capital to assistance manage your cyberspace worth and investment accounts. I log in almost every 24-hour interval to check on my investment. It'due south a great site for DIY investors.

The following two tabs change content below.

- Bio

- Latest Posts

Joe started Retire by forty in 2010 to figure out how to retire early on. Afterwards 16 years of investing and saving, he achieved fiscal independence and retired at 38.

Passive income is the key to early retirement. This yr, Joe is investing in commercial real estate with CrowdStreet. They have many projects beyond the USA so check them out!

Joe besides highly recommends Personal Uppercase for DIY investors. They have many useful tools that will aid you attain financial independence.

Get update via email:

Sign up to receive new manufactures via e-mail

We hate spam simply as much as yous

Source: https://retireby40.org/invest-401k-or-roth-ira/

0 Response to "Can You Contribute to an Ira and a 401k"

Post a Comment